One of our all-time favorite bloggers, Julie Ferguson of Workers’ Comp Insider, hosted the most recent Health Wonk Review – the “why hasn’t spring sprung?” edition. Maybe Julie just needs to move to Colorado… here on the Front Range, we’re definitely starting to see signs of spring – today was a beautiful sunny day,… Read more about Most Americans Might Not See Big Premium Hikes, But The Individual Market Is Different

Archives for March 2013

Healthcare Social Media Review: Which Tools Work Best For Your Patients?

Welcome to the HealthCare Social Media Review, where you’ll find all sorts of articles on the intersection of healthcare and social media. Over the years, we’ve found social media to be an excellent way to interact with our peers, colleagues, and clients – first with our blog, and now increasingly through Google + (Jay, Louise), Twitter (Jay, Louise), and Facebook. I relied heavily on Twitter when I was looking for articles to include in this HCSM Review, and all of the social media platforms we use are excellent resources when we’re looking for like-minded people or relevant, timely information on a particular topic. We’re honored to be hosting this edition of the HCSM Review. The blog posts included here are all written by people who have a strong social media presence, and we’ve included links to their Twitter, Facebook or Google+ pages so that you can follow them too.

To start things off, we have an excellent article from Nina Dunn (@Spector_health), explaining that we need to get back to basics with social media use in healthcare. Rather than focusing on the negatives (it changes too fast! There are no clear guidelines for how to use it! HIPAA!, etc.), Nina encourages healthcare providers to focus instead on the ways that social media can be beneficial. She notes that just because a platform exists doesn’t mean that you have to use it (ie, you don’t need to be on every social media channel all at once), and that it’s important to know your audience and target your social media presence accordingly. Good content is king (that rule never changes), and social media marketing might require a different mindset when it comes to measuring success – but that’s not a reason to avoid it. All in all, a great read, and a perfect tone for the Healthcare Social Media Review…

David Harlow of HealthBlawg gives us a perfect example of how social media can be very useful in terms of gathering information and engaging people in real time to solve problems. The Office of the National Coordinator (ONC) for Health IT issued a request for information (RFI) on interoperability, asking “What specific HHS policy changes would significantly increase standards based electronic exchange of laboratory results?” The problem appears to basically hinge on the fact that labs receive no financial incentives to make their reports interoperable and compliant with EHR meaningful use standards (medical offices do have a financial incentive to do so). Keith Boone (@motorcycle_guy) blogged about the question, and then the power of social media took over thanks to retweets and […]

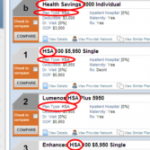

You Have To Have An HSA Qualified Health Plan In Order To Set Up An HSA

It’s tax season, and that always correlates with an increase in questions about HSAs. We always get several calls at this time of year from people who want to set up just an HSA by itself and are wondering how to go about that, and we’ve even had people call and tell us that their accountant told them to go set up an HSA because it would be an excellent way to get an additional tax deduction.

HSAs (health savings accounts) are indeed a great way to get an above-the-line tax deduction. They’re also a great way to save for future medical expenses and/or retirement. But it’s not as simple as just setting one up and contributing money. You have to have an HSA qualified high deductible health plan in place in order to be able to contribute money to an HSA. Not all high deductible health insurance policies are HSA qualified. The IRS has very specific guidelines in terms of how HSA qualified HDHPs have to be structured, and if a plan meets those guidelines, it will be labeled as such in the marketing materials.

Look at the picture below:

“PPO (0) – HMO (0)” ??? That’s confusing too! PPO and HMO are network types and HSA qualified has nothing to do with networks. HSA qualified plans can be PPO or HMO. In Colorado, all individual health insurance is PPO, except for Kaiser Permanente. They’re the only individual/family HMO.

To give an example, our family had an HSA qualified HDHP for several years, and we contributed to our HSA during those years. But in 2011, we switched to a Core Share plan from Anthem Blue Cross and Blue Shield. It’s less expensive than Anthem’s HSA qualified plans (and less expensive than most of the other plans we looked at as well), and even though it’s a high deductible plan, it doesn’t meet the requirements for being HSA qualified. The maximum allowable out-of-pocket expense limit for a family on an HSA qualified plan is $12,500 in 2013, and our plan has a $15,000 maximum out-of-pocket exposure for a family. So even though the policy has a high deductible, covers preventive care before the deductible, doesn’t have copays, and generally meets all of the other requirements, the higher out-of-pocket limit means that we cannot contribute money to our HSA unless we switch back to an HSA qualified health plan in the future.

That same IRS link also explains how you can switch to an HSA qualified health plan anytime up until […]

Cavalcade of Risk And Social Media Use In Healthcare

The 179th edition of the Cavalcade of Risk is live now, over at My Personal Finance Journey, with posts from several notable bloggers. I thought this post from David Williams was especially interesting, focusing on social media and healthcare providers: a topic about which basically all providers needs to educate themselves. (And it ties in… Read more about Cavalcade of Risk And Social Media Use In Healthcare

Welcoming Submissions for the HealthCare SocialMedia Review

We’re excited to host the next HealthCare SocialMedia Review (#hcsm) on Wednesday, March 27th. No specific theme other than articles relating to social media and healthcare/medicine. Please email submissions to Louise: louisen78 at gmail dot com by Monday, March 25th at 6PM MDT. Please include the following information: Email Subject: HealthCare SocialMedia Review Blog Title:… Read more about Welcoming Submissions for the HealthCare SocialMedia Review

Could Cash-Only Clinics Be A Viable Solution For The Uninsured?

David Williams did an excellent job with the most recent Health Wonk Review, hosted at his Health Business Blog. There are lots of great articles about a wide range of healthcare policy topics, so be sure to check it out. One of my favorite posts in this edition comes from Wright on Health. Brad Wright… Read more about Could Cash-Only Clinics Be A Viable Solution For The Uninsured?

Let Medicare Negotiate Drug Prices And The Government Can Afford Subsidies

Right in the middle of the sequestration mess seems like a good time to discuss the subsidies that are going to be a major part of the ACA starting next year. As of 2014, nearly everyone in the US will be required to have health insurance, and all individual health insurance will become guaranteed issue. There are concerns that premiums in the individual market might increase significantly, but for many families the subsidies enacted by the ACA will help to make coverage more affordable. The subsidies will be available to families earning up to 400% of the federal poverty level; the premium assistance will be awarded on a sliding scale, with the families on the upper edge of that income threshold receiving the smallest subsidies.

Right in the middle of the sequestration mess seems like a good time to discuss the subsidies that are going to be a major part of the ACA starting next year. As of 2014, nearly everyone in the US will be required to have health insurance, and all individual health insurance will become guaranteed issue. There are concerns that premiums in the individual market might increase significantly, but for many families the subsidies enacted by the ACA will help to make coverage more affordable. The subsidies will be available to families earning up to 400% of the federal poverty level; the premium assistance will be awarded on a sliding scale, with the families on the upper edge of that income threshold receiving the smallest subsidies.

But how much will those subsidies cost the taxpayers? How will a government that is so cash-strapped that it’s curbing spending on programs like Head Start and special education be able to fund the subsidies called for in the ACA?

Last summer, the CBO estimated that the exchange subsidies will cost $1,017 billion over the next ten years. Undoubtedly a large sum, but probably necessary in order to make guaranteed issue health insurance affordable for low- and middle-income families.

That sum is partially offset by the CBO’s projections of $515 billion (over the next ten years) in revenue from individual mandate penalties (fines imposed on non-exempt people who opt to go without health insurance starting in 2014), excise tax on “Cadillac” group health insurance policies, and “other budgetary effects” enacted by the healthcare reform law.

That leaves us with $502 billion. Not an insignificant sum of money even when […]

The Expansion Of Medicaid Primarily Targets The Uninsured Population

[…] I would say that another possible explanation is that the population that is most likely to be impacted by Medicaid expansion is the population more likely to be uninsured prior to the Medicaid expansion. The bar graph on page 2 of this Kaiser Family Foundation document shows significantly higher numbers of uninsureds in the population that earns less than 200% of FPL, compared with the population that earns more than that amount. So it’s likely that Medicaid expansion is most likely to cover people who didn’t previously have insurance. For the reasons Jason detailed, I would agree that it’s unlikely that very many people who already have private health insurance would choose to drop their private coverage and enroll in Medicaid, unless Medicaid coverage were to become as good as private health insurance.

Will Marketplace Customer Service Be On A Par With Private Industry?

One of our clients recently told us about a health insurance plan that was being marketed to him, and we were curious enough to want to look into the situation further. In a nutshell, it’s not a discount plan, not a mini-med, and not a traditional limited-benefit indemnity plan. All of those plans should be avoided in general, and the ACA has sort of skirted around them a bit: numerous mini-meds have been granted temporary waivers in order to continue to operate, discount plans aren’t addressed by the ACA at all (and aren’t regulated by most state Division of Insurance departments either, since they aren’t actually insurance), and limited benefit indemnity plans are exempted from ACA rules (although people who have them will likely have to pay a penalty for not meeting minimum benefit requirements).

Anyway, the plan that was marketed to our client resembled traditional health insurance, but was very convoluted and sold with numerous riders to cover all sorts of different scenarios. The brochure was 27 pages long and included numerous detailed examples showing how awesome the marketed coverage was when compared with “traditional major medical.” It noted that the plan isn’t subject to ACA mandates, and the policy is still being marketed with a $5 million lifetime maximum. When I spoke with an agent for the plan (a captive agent, of course – plans like that are never marketed by brokers who have access to other policies), he told me that the policy will not be guaranteed issue next year, and that they aren’t concerned about the potential penalties that their clients will have to pay starting in 2014 for not having ACA-compliant coverage. His reasoning (and the marketing pitch that they’re making to their clients) is that their premiums will be so much lower than ACA-compliant plans that their clients will save enough money to more than make up for the penalty (currently their premiums were roughly the same as those of reputable health insurance policies).

In short, everything about this policy sounded sketchy.

A rather lengthy Google search didn’t bring up much in the way of regulations pertaining to this sort of issue. I remembered my efforts in the fall of 2011 to get specific details about regulations regarding mini-meds… and I wasn’t encouraged. At the time, the Colorado Division of Insurance wasn’t aware of a solution to the problem our client was facing (although to give them credit, I was able to speak with someone as soon as I called them). They referred me to HHS, where I had to leave a voice mail. The outgoing message said that someone would get back to me within five business days, but that was a year and a half ago and I’m not holding my breath for a reply. I also left a message for the National Association of Insurance Commissioners (NAIC) about the issue and never heard back from anyone there. We ended up getting the client onto an Anthem Blue Cross Blue Shield plan, but we never heard back from any of the government agencies we contacted regarding his mini-med situation.

A rather lengthy Google search didn’t bring up much in the way of regulations pertaining to this sort of issue. I remembered my efforts in the fall of 2011 to get specific details about regulations regarding mini-meds… and I wasn’t encouraged. At the time, the Colorado Division of Insurance wasn’t aware of a solution to the problem our client was facing (although to give them credit, I was able to speak with someone as soon as I called them). They referred me to HHS, where I had to leave a voice mail. The outgoing message said that someone would get back to me within five business days, but that was a year and a half ago and I’m not holding my breath for a reply. I also left a message for the National Association of Insurance Commissioners (NAIC) about the issue and never heard back from anyone there. We ended up getting the client onto an Anthem Blue Cross Blue Shield plan, but we never heard back from any of the government agencies we contacted regarding his mini-med situation.

So back to our current questions about the sketchy-sounding health insurance being marketed to our client. I contacted HealthCare.gov via Twitter but got no response. I called the Colorado Division of Insurance and was told that I should send in an email with the specifics. I did that on Wednesday and haven’t heard anything back from them yet. I called them this morning to follow up, and they told me that they had received my email but didn’t know to whom it had been assigned yet – this is two days after I sent it, so I would assume that perhaps the employees there are overworked and understaffed. I didn’t contact the national HHS office again, because I didn’t feel like wasting my time any further. However, I did send an email on Friday morning to the regional HHS office in Denver, so hopefully I’ll hear back from them sometime soon.

I’m also hopeful that I’ll hear back from the Colorado DOI sometime next week. They usually end up being a helpful – and local – resource, even if we have to wait a few days. Once we get some more information, I’ll write a follow-up post about how an individual carrier is apparently able to operate entirely outside the regulations of the ACA.

But for now, I’m struck by how difficult it can be to obtain information from a government agency, or even speak with a real person as opposed to just leaving a message or sending an email that may or may not ever get read. I know that private companies aren’t always shining examples of customer service, but I can’t imagine calling the claims or customer service number on the back of our Anthem Blue Cross Blue Shield card and being told […]