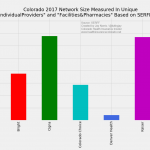

The size of insurers’ provider networks has been a headline grabber for the last few years, and there are some nascent efforts underway to make it easier to compare plans based on network size. Obviously, it’s in consumers’ best interest to search for specific providers if that’s a factor in their decision-making process, but what… Read more about Colorado Individual Market Network Size Rating Based on SERFF Data

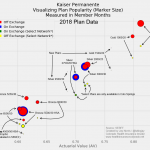

Visualizing Kaiser CO 2018 Plan Popularity, Premium, and AV

Have you ever wondered how popular your health plan is, compared with the other available options? Curious about how your plan’s actuarial value (a measure of the percentage of average medical costs it covers) compares with the premium, and how that metric stacks up against other plans? View Full Size PDF Here’s a summary… Read more about Visualizing Kaiser CO 2018 Plan Popularity, Premium, and AV

The latest Health Wonk Review is up!

Trying to keep up with healthcare policy? The Health Wonk Review is hot off the press from our friend David Williams at the Health Business Blog. Enjoy!

Joe Paduda has an excellent Health Wonk Review

It’s a crazy time in healthcare and even the biggest health wonks are struggling to keep up. Get up to speed with the concisely written Health Wonk Review from our friend Joe Paduda. Hot off the press.

Connect for Health Colorado and the OIG Audit Report

On December 27, the U.S. Department of Health and Human Services’ Office of Inspector General (OIG) released an audit report (the full report is here) regarding Connect for Health Colorado’s use of federal start-up funding. This funding was provided for state-run exchanges to get their operations up and running in 2013 and 2014. To make a… Read more about Connect for Health Colorado and the OIG Audit Report

PEAK Issues

As of now, it appears that PEAK has various errors. If you’ve had coverage through PEAK in the past, submitting a financial determination for 2017 also re-determines your 2016 financial eligibility. This can cause major problems with your 1095-A, your billing, and your insurance plan. **NO Confirmed Fix Yet** I will update this page when there… Read more about PEAK Issues

Short and Sweet Health Wonk Review

Jason Shafrin has the latest Health Wonk Review at Healthcare Economist. You’ll find some of the greatest writing by healthcare experts about health insurance, pharmaceuticals, the ACA, mental health, and physician pay.

If you’re facing the subsidy cliff, enroll through Connect for Health Colorado

The Canon City Daily Record published a story this week highlighting how expensive health insurance is in the Colorado mountains, and how few carriers offer coverage in the mountains. Despite the fact that the Division of Insurance combined some rating areas to alleviate the problem ahead of the 2015 open enrollment period, rates for 2016… Read more about If you’re facing the subsidy cliff, enroll through Connect for Health Colorado

Connect for Health Colorado and non-resident brokers

At today’s Connect for Health Colorado board meeting, there was some discussion over the issue of whether or not Colorado’s exchange should work with out-of-state web brokers. Here’s the background on the issue, and I want to clarify my position in case there was any confusion. I’ve been a local broker in Colorado for 14… Read more about Connect for Health Colorado and non-resident brokers

Healthblawg has a great Health Wonk Review

Sit down with David Harlow for the Turkey Edition of the Health Wonk Review. It’s a full helping of educational and though provoking posts.

Assigning an agent/broker with Connect for Health Colorado

redirected

The Coming Storm Over the 340B Rx Drug Discount Program

We’ve invited Healthcare Lighthouse CEO Billy Wynne to share his posts with us. Today’s piece addresses the forthcoming regulation that will likely make sweeping changes to the 340B program. Keep an eye out for additional pieces in the coming weeks and be sure to check the Lighthouse Blog for some of our posts. Beneath the glare… Read more about The Coming Storm Over the 340B Rx Drug Discount Program

Infographic – Affordable Care Act and How Individual Health Insurance is Changing in 2014

A quick overview of how individual health insurance will change in 2014 due to the Affordable Care Act (ACA).

A Little Flurry of Snow in Northern Colorado Today!

Just enough snow came through the Fort Collins area for the kids to plow… and mow. We’re hoping the mountains get a lot for skiers and snowboarders. We put the kids to work in the yard. Plowing…

And mowing…

Here is a video of the front end loader in action plowing the snow off of the porch! It was a gift from a friend and is their favorite toy…

Rocky Mountain Health Plans 2013 Rate Increase Announced

Rocky Mountain Health Plans announces the 2013 new business rate increase for the “SOLO” individual/family health insurance plans in Colorado is 18%. As with all carriers, for existing clients on open plans, rate changes may be different due to age attainment and trend. Carriers may adjust rates differently for closed plans effective January 1, 2013.

RMHP posted the disclosure of the increase for new and renewing business on healthcare.gov.

For clients who pay monthly:

- January renewals were mailed Friday, November 30, 2012.

- February renewals will be mailed the end of December.

- March renewals will be mailed the end of January.

No 2013 Rate Increases for Cigna or Anthem Blue Cross of Colorado

Both Cigna and Anthem Blue Cross of Colorado report no rate increases on new business in Colorado. However, for existing clients on open plans, rates may change due to age attainment and trend. Carriers may adjust rates for closed plans effective January 1, 2013.

Kaiser Permanente 2013 Rate Increase Announced

Kaiser Permanente announces the average 2013 rate increase for individual/family health insurance in Colorado was 11%.

I wish my health insurance _____________?

I understand the trade off we got when we switched to a really inexpensive high deductible plan when even our high deductible HSA qualified plan was too rich and expensive. So I wish my health insurance had a monthly credit card billing option. Our current health insurance company, Anthem Blue Cross of Colorado used to have it, like most health insurance companies did. But then, like most other companies also did, they stopped offering that as an option about a year ago.

What would you change about your health insurance company or plan? It could be the coverage, billing, customer service, anything…

2012 Obamacare Premium Rebates (Infographic)

Did you receive a health insurance premium rebate this year? If so, how much was it? We created a simple visualization of how the PPACA (Obamacare) health insurance premium rebates break down between the individual/family, small group and large group markets and how Colorado’s rebates compared to the national average.

")

No 2013 CoverColorado Assessment

CoverColorado announced that there will be no assessment in 2013 on Colorado health insurance carriers. The 2012 assessment was roughly $3.79/month/contract for individual/family insureds.

Anthem Blue Cross of Colorado has also announced that their membership this year was higher than expected this year. They were making up for a shortfall by charging $4.36/month/contract in 2012. Due to the higher enrollment, Anthem BCBS has enough funding to satisfy December without billing subscribers a CoverColorado assessment.

Snow in Colorado Last Night, But Not Very Much

We just got a little bit of wet, sticky snow in Colorado last night; just enough for a little snowman in the morning. Matt made the snowman all by himself! Most of the snow in the yard has melted this evening, but not the snowman!

Colorado Selects Kaiser Permanente As Its Benchmark Health Insurance Plan

Last December, HHS made it clear that they were giving states a lot of flexibility in determining what plan would serve as the benchmark for the state’s “essential benefits” for individual and small group health insurance policies that would be sold starting in 2014.

After months of consideration, Colorado has selected Kaiser Permanente’s small group plan as a benchmark. This is the largest small group plan in the state, with almost fourteen thousand members, and was selected by a group of officials from the Colorado Division of Insurance, the Governor’s office, and the health benefits exchange. The Division of Insurance will be taking comments until next Monday before making a final announcement, and you can contact them by email (ehb@dora.state.co.us) if you’d like your comments to be considered.

The Kaiser plan covers services in the ten areas that are required by the PPACA (ambulatory patient services, emergency care, hospitalization, maternity and newborn care, mental health and substance abuse services, prescription medications, rehabilitative services, lab work, preventive care/disease management, and pediatric care), which means that it will serve as a benchmark for services in those areas without the DOI having to add additional coverage minimums. In addition, the Kaiser plan was generally considered to be a good balance between comprehensive coverage and affordable coverage. It’s not the most comprehensive policy out there (the much maligned “Cadillac plans” offer more benefits), but it provides […]

Low Deductible Still Required To Waive CSU Student Health Insurance

I’ve been getting a lot of questions from CSU graduate and international students. I just confirmed with the Colorado State University (CSU) Health Network that they’re not budging (much) on the requirement that graduate and international students have a $500 deductible if they want to waive the CSU Student Health Insurance. The person I talked to did mention they might allow a $1000 deductible if the student can prove sufficient financial resources to pay such a large bill.

Meanwhile, the CSU Student Health Insurance Plan has a policy year limit of $250,000 per accident/illness. It’s much better than a mini-med, but they still have a reputation for getting maxed out. I asked if they’ve ever had a student hit the limit (like has happened at other schools), and she said she could only think of one minor case when the student was able to wait until the next calendar year when the benefits started over.

The CSU Health Network is a really great organization though, if it weren’t for the low cap on benefits. They have top notch providers and are very friendly and helpful. And on January 1, 2014, even university health insurance plans will be required to not have a cap on benefits because of the Affordable Care Act.

I Thought Insurance Companies Couldn’t Decline Due To Pre-Existing Health Conditions Anymore?

One of the most common questions lately: I was declined for health insurance due to a pre-existing health condition. I thought insurance companies couldn’t look at our pre-existing health conditions anymore because of [the PPACA] ObamaCare?”

Colorado Health Insurance CO-OP Receives Loan From HHS

At the end of July, the first of Colorado’s health insurance CO-OP plans got a $69 million loan from HHS as part of a push by the ACA to develop consumer-owned-and-operated health insurance plans (“CO-OP” is short for Consumer Oriented and Operated Plans). The CO-OP is sponsored by Rocky Mountain Farmers Union and the bulk of the loan from HHS will be put in reserve to fund claims expenses for initial enrollees. As premium dollars are collected, the loan will be paid back to HHS.

Colorado Senator Irene Aguilar introduced a bill last year to create a state-wide Colorado health insurance co-op, but the bill was tabled in May 2011 after passing its second reading in the Senate.

The new CO-OP being created with the loan money will be especially focused on rural areas of Colorado – which are generally underserved in terms of health insurance options. In addition, residents in rural areas are often already familiar with the concept of co-ops for other services like utilities. So a Colorado health insurance plan that is owned and operated by its members should be an especially good fit.

The CO-OP will begin marketing plans next fall with policy effective dates starting January 1, 2014, and is hoping to enroll 10,000 Colorado residents in its first year. Unlike most commercial health insurance plans available in Colorado, the CO-OP will be able to direct profits back into the plan in the form of lower premiums and/or higher quality service rather than sending profits to shareholders. And while most health insurance carriers that do business in Colorado are multi-state organizations, the CO-OP will be a local plan based here in Colorado (Rocky Mountain Health Plans is another example of a local, non-profit health insurance option for people in Colorado).

The CO-OP expects to be available both through the Colorado Health Benefits Exchange (aka “the exchange”) and also via independent health insurance brokers and agents. An innovative new health insurance product – especially one that strives to serve populations that are underserved by our current health insurance industry – is good news for Colorado, as it should foster more competition among the existing health insurance carriers in the market. Congratulations to Rocky Mountain Farmers Union for the approval from HHS for the loan to get the CO-OP going!